How to Retire in 21 Years and 12 Days

Do you wish you had more time to do what you love rather than what someone else tells you to do?

You can. Even starting with $0, you can reach financial independence in approximately 21 years and 12 days. The equation is easy…

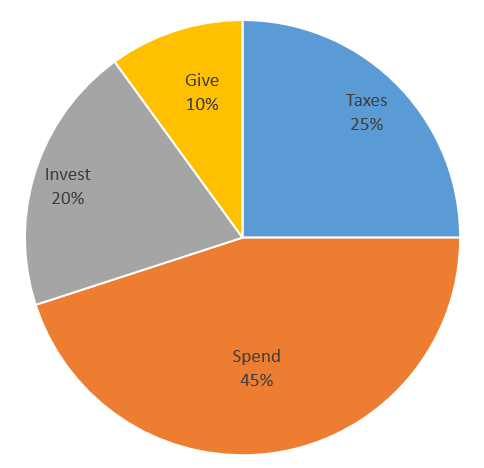

Take your gross income and break it down into the following:

-

Give 10% away (optional)

-

Pay 25% in taxes (not optional, unfortunately…)

-

Spend 45% on whatever you want

-

Invest 20% into a diversified portfolio of stocks/bonds

No matter how much you make each year, if you followed that formula for 21 years and then continued the same level of spending* forever - you would be able to live off of the passive income generated by your investment portfolio for the rest of your life.

And at the end of your days, you would be able to give the entire investment portfolio to your kids, church, charity, or whomever you wanted.

Here's how it works...

Let’s say we have a fictional couple named Jim and Jane.

Jim and Jane earn a gross (meaning before taxes, etc.) household income of $60,000 per year. They give $6,000 away and pay about $15,000 per year to the U.S. Government. That leaves them with $39,000 to either spend or invest. They invest $12,000 of it and spend the remaining $27,000.

If they continue to spend $27,000* for the rest of their lives, they would need a $540,000 investment portfolio to live on the dividends and interest produced by the portfolio each year (about 4% per year).

Starting from an investment portfolio of $0, as long as Jim and Jane continued to invest 20% of their gross income ($12,000 per year) and were able to get a 7% rate of return*, they would be able to retire in 21 years and 12 days.

What About Different Income Levels?

Gross Income

| Taxes

| Giving

| Spending

| Investing

| Retire in...

|

|---|---|---|---|---|---|

$40,000

| $10,000

| $4,000

| $18,000

| $8,000

| 21 years 12 days

|

$80,000

| $20,000

| $8,000

| $36,000

| $16,000

| 21 years 12 days

|

$100,000

| $25,000

| $10,000

| $45,000

| $20,000

| 21 years 12 days

|

Now, I understand there are going to be some objections to this… so let’s address those now.

Objection #1: How can Jim and Jane live on only $27,000 per year?

Jim and Jane can live quite a posh life on $27,000. They can buy organic foods, enjoy fancy meals with their friends (wine included), take a nice vacation each year, and even buy an overpriced coffee beverage from Starbucks on the occasion. And they don’t even have to clip coupons!

Their secret is not that they cut every single corner, but they focus on the big wins. While most American households spend 55% of their monthly income paying for their giant house and brand new cars, Jim and Jane only spend about 30% on these things.

That difference in and of itself is just about enough to cover their 20% savings rate without them having to make any additional “sacrifices”. They can still live quite fancy lifestyles after abiding by the following rules:

#1 - Never borrow more than 100% of your gross income (in their case, $60,000) to buy a house. So they put a 20% down payment on a $72,000 house and borrowed $60,000 for their house.

#2 - Never own cars whose combined initial cost is in excess of 10% of your gross income. Jim and Jane both drive very modest vehicles that cost a total of $6,000.

Objection #2: How can Jim and Jane earn a 7% rate of return after inflation?

There are lots of ways. Many people have achieved rates of return well in excess of this. I’ve estimated 7% because that is the rate of return that the vast majority of people can achieve without having any fancy real estate or stock-picking skills…

7% is the long-term inflation-adjusted rate of return for the U.S. stock market. Investing in the stock market doesn’t take much more than a few mouse clicks and 10 minutes of a person’s day.

Investing really isn’t that complicated. If you want to get started today, you can get your first account open in about 8 minutes and start following one of my 10-Minute Portfolios. They are each designed to be low-cost, maximally diversified and only take about 10 minutes per year to manage. And the best part? You’ll outperform 90% of investment “experts” without any special knowledge or training.

10-Minute Portfolios

Below is the performance of the 10-Minute 70/30 Portfolio. Since 1976, this portfolio has turned $100 to nearly $6,000. It has outperformed the overall U.S. stock market despite having significantly less volatility. That's something that is incredibly difficult to accomplish!

I have a free investment newsletter that you can follow along with this portfolio or any of the other 3. It'll only take you about 10 minutes to subscribe and get started investing!

The 10-Minute Portfolio 70/30

Do you want to be financially free in 21 years and 12 days? You can. It may take some initial lifestyle changes, but you can do it! Stay committed to your goal and keep socking away the cash!

*Adjusted for inflation each year… which means Jim and Jane could increase their spending by about 2-3% per year to keep up with the rising costs of goods.

**The long-term inflation-adjusted rate of return of the U.S. stock market. An investor following one of the 10-minute portfolio would have achieved even better than that since 1976.